Resilience-Adjusted Credit Risk: Operationalising climate adaptation in financial decision-making

26 May 2026 – A report by CISL’s Banking Environment Initiative (BEI) outlines an approach to embed physical risk, insurance, and resilience into financial decision-making.

Download the Resilience-Adjusted Credit Risk report:

About

The report, developed by CISL’s Banking Environment Initiative (BEI), highlights how physical climate risk is accelerating faster than financial systems are adapting to it, exposing a critical gap in traditional credit risk frameworks that rely on historical data, assume stable insurance coverage, and overlook the value of adaptation and resilience investments. It introduces the Resilience-Adjusted Credit Risk (RACR) framework, a forward-looking approach that integrates physical risk exposure, insurance adequacy, and resilience measures into core credit metrics such as probability of default and loss given default. Designed to be practical and scalable, RACR enables financial institutions to better assess and price climate risk while supporting clients in managing it, while also setting out a broader call for collaboration across banks, insurers, investors, and regulators to strengthen financial system resilience.

Physical climate risk is materialising faster than financial systems are adapting to it. The decade 2015–24 was the warmest on record and flood-related disasters have risen 134 per cent since 2000. Yet current credit risk frameworks remain calibrated on historical data, mostly assume insurance as a static condition of lending, and have no mechanism to recognise investment in adaptation and resilience (A&R) as a credit-positive variable. The result is a financial system that is accumulating physical climate risk faster than it is pricing it and actively directing capital into possible future stranded assets.

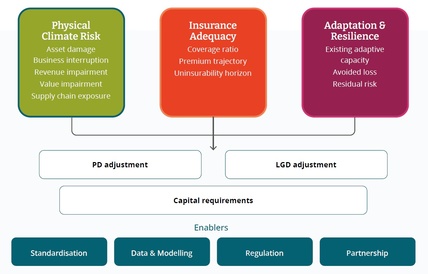

This report proposes the Resilience-Adjusted Credit Risk (RACR) framework: a structured approach to integrating physical climate risk, insurance adequacy and A&R investment into standard credit assessment, adjusting the core metrics of probability of default (PD) and loss given default (LGD) to reflect both borrower exposure to physical hazards and their capacity to manage and reduce that exposure.

Figure 1: Resilience-Adjusted Credit Risk framework

The problem is structural. Banks are aware of the challenge and increasingly engaged with it, but face six compounding barriers: regime gaps in prudential frameworks; a revenue paradox in which A&R investment benefits are not captured; low observed climate-related bad debts that understate forward-looking risk; attribution failures that obscure climate losses within standard risk categories; a horizon mismatch between credit tenors and the timescale of physical risk and A&R materialisation; and a growing insurance blind spot as coverage withdraws from high-risk markets. These barriers are self-reinforcing: invisible losses suppress urgency, which suppresses investment, which perpetuates the absence of evidence.

The RACR framework is a conceptual scaffold. Empirical calibration is a priority for future research. What this report establishes is the architecture and the urgency of beginning to build it.

Citing this report:

University of Cambridge Institute for Sustainability Leadership (CISL). (2026). Resilience-Adjusted Credit Risk: Operationalising climate adaptation in financial decision-making. Cambridge, UK: Cambridge Institute for Sustainability Leadership.